Forum adverts like this one are shown to any user who is not logged in. Join us by filling out a tiny 3 field form and you will get your own, free, dakka user account which gives a good range of benefits to you:

No adverts like this in the forums anymore.

Times and dates in your local timezone.

Full tracking of what you have read so you can skip to your first unread post, easily see what has changed since you last logged in, and easily see what is new at a glance.

Email notifications for threads you want to watch closely.

Being a part of the oldest wargaming community on the net.

If you are already a member then feel free to login now.

Seaward wrote: I'll continue to disagree that the Heritage Foundation speaks for the entirety of the Republican Party, then or now, just as I'd disagree that the Center for American Progress speaks for the Democratic Party.

I'm unaware of any actual Republican legislative proposals from history that bore a resemblance to the ACA, though those would make a far stronger argument.

No, it doesn't speak for all Republicans, but there's just no point denying that there is an incredibly strong link between the Heritage Foundation and the Republican party. The Heritage Foundation's role is basically to develop and then advocate the next generation of conservative policy. So when you have a policy developed at the Heritage Foundation, that is a market based solution that fits conservative ideology, that Republican leaders then suggest as a form of reform for the next couple of decades, well it's pretty safe to say that's something the Republican Party generally favoured.

And so when the Republican party began it's effort to prevent Obamacare, and then ACA ended up being something the Republican party in general had been in favour of, and Republicans continued their campaign with increased vigour, well it's worth pointing out the cynicism in their position.

That's all. That's all the origins in the Heritage Foundation mean. It's just one piece of the overall story about how cynical Republican opposition to this bill has been.

It doesn't mean Republicans own the current bill. All it means is that Republicans own their response to the bill, and that response was absolutely and utterly intellectually bankrupt, a product of nothing but blatant political opportunism. Which should tell us all something about the amount of truth in the 'ACA is disaster' articles released by the conservative noise machine for the last four years.

Automatically Appended Next Post:

Seaward wrote: No. Boehner's a guy who can actually put legislation on the floor of the House.

Well, unless it's a bill to continue funding government and he's afraid of the Tea Party, then the poor orange man is incapable of putting up legislation.

This message was edited 1 time. Last update was at 2013/11/04 08:55:25

“We may observe that the government in a civilized country is much more expensive than in a barbarous one; and when we say that one government is more expensive than another, it is the same as if we said that that one country is farther advanced in improvement than another. To say that the government is expensive and the people not oppressed is to say that the people are rich.”

Adam Smith, who must have been some kind of leftie or something.

How Insurers Are Hiding Obamacare Benefits From Customers

Donna received the letter canceling her insurance plan on Sept. 16. Her insurance company, LifeWise of Washington, told her that they'd identified a new plan for her. If she did nothing, she'd be covered.

A 56-year-old Seattle resident with a 57-year-old husband and 15-year-old daughter, Donna had been looking forward to the savings that the Affordable Care Act had to offer.

But that's not what she found. Instead, she'd be paying an additional $300 a month for coverage. The letter made no mention of the health insurance marketplace that would soon open in Washington, where she could shop for competitive plans, and only an oblique reference to financial help that she might qualify for, if she made the effort to call and find out.

Otherwise, she'd be automatically rolled over to a new plan -- and, as the letter said, "If you're happy with this plan, do nothing."

If Donna had done nothing, she would have ended up spending about $1,000 more a month for insurance than she will now that she went to the marketplace, picked the best plan for her family and accessed tax credits at the heart of the health care reform law.

"The info that we were sent by LifeWise was totally bogus. Why the heck did they try to screw us?" Donna said. "People who are afraid of the ACA should be much more afraid of the insurance companies who will exploit their fear and end up overcharging them."

Donna is not alone.

Spoiler:

Across the country, insurance companies have sent misleading letters to consumers, trying to lock them into the companies' own, sometimes more expensive health insurance plans rather than let them shop for insurance and tax credits on the Obamacare marketplaces -- which could lead to people like Donna spending thousands more for insurance than the law intended. In some cases, mentions of the marketplace in those letters are relegated to a mere footnote, which can be easily overlooked.

The extreme lengths to which some insurance companies are going to hold on to existing customers at higher price, as the Affordable Care Act fundamentally re-orders the individual insurance market, has caught the attention of state insurance regulators.

The insurance companies argue that it's simply capitalism at work. But regulators don't see it that way. By warning customers that their health insurance plans are being canceled as a result of Obamacare and urging them to secure new insurance plans before the Obamacare launched on Oct. 1, these insurers put their customers at risk of enrolling in plans that were not as good or as affordable as what they could buy on the marketplaces.

TPM has confirmed two specific examples where companies contacted their customers prior to the marketplace's Oct. 1 opening and pushed them to renew their health coverage at a higher price than they would pay through the marketplace. State regulators identified the schemes, but they weren't necessarily able to stop them.

It's not yet clear how widespread this practice became in the months leading up to the marketplace's opening -- or how many Americans will end up paying more than they should be for health coverage. But misleading letters have been sent out in at least four states across the country, and one offending carrier, Humana, is a company with a national reach.

"If you're an insurance company, you're trying to hang onto the consumers you have at the highest price you can get them," Laura Etherton, a health policy analyst at the U.S. Public Interest Research Group, told TPM. "You can take advantage of the confusion about what people get to have now. It's a new world. It's disappointing that insurance companies are sending confusing letters to consumers to take advantage of that confusion. The reality is that this could do real harm."

Before Obamacare, Donna paid a $724 monthly premium for $10,000 deductible, catastrophic health coverage from LifeWise, a subsidiary of the state's Blue Cross/Blue Shield affiliate. She asked that TPM withhold her last name because she was disclosing personal financial information.

The Sept. 16 letter from LifeWise told her that her existing plan was being canceled to comply with the new requirements of Obamacare and that she would automatically be rolled over into a new plan that was the "closest match" to her old plan. "If we don't hear from you, we'll automatically move you to this plan and you'll be covered starting January 1, 2014," the notice read.

Under the new LifeWise plan, Donna would have to pay more than $1,000 a month, a nearly $300 per month increase and a huge hit for a family with an income around $40,000. It was bare-bones coverage by ACA standards, with a $6,350 deductible.

The letter, which you can read here, made no mention of the insurance marketplace that was about to open, where she could shop around for other options. It did mention that she might qualify for financial help in the form of a tax credit but the onus was on Donna to call the insurer for more information.

Fast forward a month, and Donna was able to log onto Washington's marketplace and shop for insurance. And what did she find? Options. A LifeWise plan with the same deductible they offered her outside the exchange was a little cheaper. Plans with a lower deductible had the same or lower premiums as the LifeWise plan. What she ended up buying was a plan through Community Health Plan of Washington with a $250 deductible.

And crucially, she also discovered she would qualify for a federal tax subsidy that would knock her monthly premium to $80. Her daughter could enroll in Medicaid, at no cost to the family.

So here's the bottom line: If Donna had taken the default option that LifeWise offered outside of the marketplace, she would have paid nearly $1,000 more per month for a worse plan than she was able to obtain on the marketplace.

A LifeWise spokesman told TPM that the Washington marketplace had done plenty of its own advertising and the company assumes that customers know they have other options. He also noted that more information was available on the company's website.

"Our experience is that our customers are already aware that they have other options in the market and that we've never had to tell them in the past that we have competitors," Eric Earling, director of corporate communications at Premera Blue Cross/Blue Shield, said. "We knew that (the marketplace) would have a robust marketing campaign for themselves and knew they didn't need any additional help from us."

As a result of the letter LifeWise sent to Donna and other customers, state regulators in Washington issued a consumer alert on Sept. 19, warning residents about the misleading information. "Don't just take what your insurance company says, make sure you shop around. You have the right to buy any plan inside the new exchange or in the outside market," Insurance Commissioner Mike Kreidler said in the alert.

But the agency doesn't have the statutory authority to stop LifeWise from sending the misleading letters, a spokeswoman told TPM. The company controls one-third of the state's 300,000-person individual health insurance market -- leaving a lot of people at risk of being duped.

"Yes, that's possible," Stephanie Marquis, the spokeswoman, said when asked if some Washingtonians could be paying much more for insurance than they could if they went on the exchange because of LifeWise's actions.

"One of our concerns has been that people don't know they have these new rights," Marquis said. "The insurance companies can manipulate or withhold that information to increase their market share. It's just really disingenuous."

Donna's experience isn't an isolated incident, however. And the wider spread the issue is, the likelier it becomes that some people have been manipulated into spending more for insurance than they should.

Kentucky fined Louisville-based Humana for sending out letters with similarly misleading information to customers in that state. They received complaints about an Aug. 21 letter that pressed customers to renew their policy now or risk increased rates under Obamacare.

But like LifeWise, Humana downplayed the fact that people could search the marketplace for other insurance options or that they might qualify for Obamacare's financial assistance, state insurance commissioner Sharon Clark, pictured, told TPM in an interview. A footnote referenced the "open enrollment period" that started Oct. 1, but didn't name the state's marketplace or the ACA's financial assistance directly.

After receiving the letter, which you can read here, some customers were badgered through phone calls to make a decision, Clark said. Of the 6,500 people who received a letter, 2,200 actually responded and gave the company their answer before they had a chance to look at what the Kentucky marketplace had to offer.

But Clark's office soon stepped in. They fined Humana $65,000 for the "misleading" information, and the 2,200 respondents were released from their obligation to Humana and freed to shop for insurance through the Obamacare marketplace starting Oct. 1.

The most troubling part of the Humana case is that the company was pushing customers into a Humana insurance plan that was more expensive than the plan Humana was selling on the Obamacare marketplace, without the financial help available under Obamcare.

Clark gave the example of a single mother with children who was urged to sign up for a Humana plan with a monthly premium of $719.86. That price is higher than any comparable plan for sale on the state's insurance marketplace, Clark said -- not to mention that the mother might have qualified for tax subsidies to help pay for it if she went through the marketplace, as Donna did.

"People don't think about insurance every day," Clark said, "and in an environment with so many changes, this has been a period of confusion and uncertainty for people."

Colorado regulators also received complaints about a similar Humana letter, dated Aug. 28 on a copy obtained by TPM, that went out to 3,400 customers in their state.

It only mentioned the Obamacare marketplace and financial help in, again, a footnote. The company wasn't fined as it was in Kentucky, but state officials forced Humana to send out an apology and a corrected letter that met the state's standards.

"The letter appeared threatening," Vincent Plymell, a spokesman for the state insurance department, told TPM. "You've got to let people know their options. You can't make it seem like they have to stick with your company."

State officials in Missouri also told TPM that they have received complaints about misleading letters from Humana and were in the process of investigating them.

Asked by TPM about the Kentucky letter that resulted in a fine, Humana senior vice president for corporate communications Tom Noland offered the following statement via email, but declined to comment further.

"In retrospect, the letter could have been more consumer-friendly and we've rewritten it with that in mind. We are continuing to work closely with the Department of Insurance to ensure our messaging is clear and not adding confusion to consumers during this period of adjustment and transition."

Clark, the Kentucky insurance commissioner, told TPM that Humana executives had told state officials that there had been "a major disconnect" between the marketing and government compliance arms of the company.

"That was the excuse they gave us," she said. "That was the rationale."

"This is a great example of the kind of consumer abuses that are typical of the insurance industry, and they're supposed to stop under the ACA," Ethan Rome, executive director of Health Care For America Now, a pro-Obamacare advocacy group, told TPM. "In this case, they're trying to get in just one more abuse."

So it seems a lot of the stories of people getting fee hikes might be just because insurance companies are trying to close their plans and shift them onto one which makes more money for them, hoping they won't actually explore their options. They'll probably be quite successful too, especially amongst those who won't want to use the exchanges because of their ideological bent, or because of fear because what they've heard from the former group.

This message was edited 1 time. Last update was at 2013/11/04 13:35:25

Looking for a club in Brisbane, Australia? Come and enjoy a game and a beer at Pubhammer, our friendly club in a pub at the Junction pub in Annerley (opposite Ace Comics), Sunday nights from 6:30. All brisbanites welcome, don't wait, check out our Club Page on Facebook group for details or to organize a game. We play all sorts of board and war games, so hit us up if you're interested.

Pubhammer is Moving! Starting from the 25th of May we'll be gaming at The Junction pub (AKA The Muddy Farmer), opposite Ace Comics & Games in Annerley! Still Sunday nights from 6:30 in the Function room Come along and play Warmachine, 40k, boardgames or anything else!

Maddermax wrote: So it seems a lot of the stories of people getting fee hikes might be just because insurance companies are trying to close their plans and shift them onto one which makes more money for them, hoping they won't actually explore their options. They'll probably be quite successful too, especially amongst those who won't want to use the exchanges because of their ideological bent, or because of fear because what they've heard from the former group.

There's not a lot of competition to be had in a market where everyone's forced to sell the same product by the government.

This, by the way, is absolutely beautiful.

My favorite part:

Schieffer: The president said in the beginning that one thing was that if you liked the health care program you had, you could keep it. We now know there was debate within the administration before he said that as to whether that was actually a promise that could be kept. Should the president not have made that statement?

Feinstein: Well, as I understand it, you can keep it up to the time — and I hope this is correct, but this is what I’ve been told — up to the time the bill was enacted, then after that, it’s a different story. I think that part of it, if true, was never made clear. It is really very unclear, right now, exactly what the situation is.

You honestly trying to claim the Heritage Foundation isn't a core element of the Republican political machine?

Core elements? No... I disagree with that.

I think all think-tanks don't really represent their favor party at all. They're all about their agenda and using their political lobbying connections.

or... Dems are running away from the PPACA because it's so unpopular. Not sure how really.... incumbents have major electoral advantages anyways. *shrugs*

What? That makes no sense given your own link. It was about the Democrats saying 'well we've been so attached to this thing we've really got no option left but to stand up for it'.

I was more alluding to the fact that the voters have real short attention spans... the failings of the PPACA is hot right now. By next November? Who knows. *shrugs* If it stays hot, then the Dems are screwed.

From its inception the ACA has lacked anyone to champion it. Obama didn't, and throughout the period in which it was written no Democrats in the House or Senate went out and meaningfully argued for its reforms or explained why they are necessary. It is genuinely possible that I've spent more time explaining the foundations of ACA than Pelosi and Reid have combined.

Holy fething hell Seb... what the feth? Did you miss all the campaign speechs.. the floor speeches... the general fething punditry throughout the crafting of this law?

Obama / Reid / Pelosi / Biden / the whole fething Demcrat caucus championed this. I know I posted plenty of youtube links supporting this.

The bill only really got passed in the first place because Democrats got themselves in to a position where running away from the bill would likely be more harmful than passing the thing. Without their favoured tactic of ineffectual cowardice available, they passed the thing, and still none of them stood up and made a serious defence of the thing.

Wait...wut? That doesn't make one iota amount of sense Seb. The Democrats needed every bit of their own party to pass it.

And you and Dogma laughed at my pass statement on how strong that Democratic party was at this time. They were all able to band together to pass this.

Nothing much has really changed. Democrats will come out in defence of ACA, targeting specific claims about how awful it is and disputing them, but still there is a complete absence of any champions of the bill.

Eh... the perceived vulnerable red-state Democrats are strategically trying to put some distance from this act. We'll see how hot this topic will be by next spring/summer, eh?

This message was edited 1 time. Last update was at 2013/11/04 15:08:36

Maddermax wrote: Strange that Massachusetts has an employer mandate but hasn't crashed horribly. Strange indeed.

Isn't it?

“The Departments’ mid-range estimate is that 66 percent of small employer plans and 45 percent of large employer plans will relinquish their grandfather status by the end of 2013,” wrote the administration on page 34,552 of the Register. All in all, more than half of employer-sponsored plans will lose their “grandfather status” and become illegal. According to the Congressional Budget Office, 156 million Americans—more than half the population—was covered by employer-sponsored insurance in 2013.

The Department referred to is Health and Human Services. The administration referred to is President Obama's.

This is the reason the employer mandate was pushed until after the midterms. A few hundred thousand cancellation letters is one thing; tens of millions is another entirely.

Seaward wrote: I'll continue to disagree that the Heritage Foundation speaks for the entirety of the Republican Party, then or now, just as I'd disagree that the Center for American Progress speaks for the Democratic Party.

I'm unaware of any actual Republican legislative proposals from history that bore a resemblance to the ACA, though those would make a far stronger argument.

No, it doesn't speak for all Republicans,

Whoa there brother... you've been fooling me.

but there's just no point denying that there is an incredibly strong link between the Heritage Foundation and the Republican party.

Really... why does this matter when debating the PPACA?

The Heritage Foundation's role is basically to develop and then advocate the next generation of conservative policy.

Well... sure. Newsflash... The Republican PARTY isn't "The Conservative" party. I think this is the crux of your confusion.

So when you have a policy developed at the Heritage Foundation, that is a market based solution that fits conservative ideology, that Republican leaders then suggest as a form of reform for the next couple of decades, well it's pretty safe to say that's something the Republican Party generally favoured.

Reasonable people can "like" certain tenets of a proposal, no matter where/who it comes from.

But you've been arguing that the PPACA is a Republican idea, so they must own up to it (and implying they ought to help fix it).

And so when the Republican party began it's effort to prevent Obamacare,

Because they didn't want any part of it.... has nothing to do with wanting the President to "fail".

and then ACA ended up being something the Republican party in general had been in favour of,

Incorrect. NOT. EVEN. CLOSE.

and Republicans continued their campaign with increased vigour, well it's worth pointing out the cynicism in their position.

*sigh*

I can see us arguing this till we're both blue in the face.

That's all. That's all the origins in the Heritage Foundation mean. It's just one piece of the overall story about how cynical Republican opposition to this bill has been.

Nope. Still reject this premise. It's an attempt to lasso the blame game onto the GOP's lap. That's all.

It doesn't mean Republicans own the current bill. All it means is that Republicans own their response to the bill,

Well... yeah.

and that response was absolutely and utterly intellectually bankrupt, a product of nothing but blatant political opportunism.

The political opportunism is there... but, that's the nature of politics. But, "intellectually bankrupt"? That's an overstatement.

Which should tell us all something about the amount of truth in the 'ACA is disaster' articles released by the conservative noise machine for the last four years.

Well... it's currently being touted as a disaster.

Ouze wrote: Uh, not really, no. I guess it does if you didn't read either the original article or the supporting one I linked. Are you trying to predicate that I said they probably don't pay payroll tax to pretend this indeed means all of their income is undeclared? Because... well, independant contractors aren't covered by payroll tax anyway.

If this discussion is going to devolve into single sentence Seaward-style dodges and intentionally-missing-the-points, I guess good luck with that.

So how would one go about paying payroll tax on an income derived from illegal means without further breaking the law? It seems you're the one who is trying to dodge my point about their illegal income by saying that they pay taxes elsewhere (sales tax etc.)

But from your article;

ACORN, the community organizing group and Republican cause célèbre, lost its federal funding last week after some of its employees were captured on video telling people they thought were prostitutes how to manipulate tax laws.

So pretty much the prostitutes can lie about their source of income, aren't being prosecuted by the IRS, but their tax documents can be used as evidence in a criminal trial against them. But you'd have us believe that they are somehow comparable with independent contractors. So who is dodging what again?

So our President is little better then a sleazy car salesman. Selling us a lemon is more important to him, then ensuring we have a product we need. If it's that much for you, I'll give you that.

Its ok. It wasn't a lie. Those people who didn't get to keep their plans because of the ACA provisions deep down really didn't like them. Or something.......

Seaward wrote: I'm not really sure what trying to pin the origin of the idea on the Republican party really gets you.

Let's pretend for a moment that one think tank does in fact represent the GOP. They pump out a gakky individual mandate idea, then do absolutely nothing with it for years. Democrats come along and go, "Hey, this idea's just gakky enough for us, let's do it." They "misspeak" relentlessly about what this plan will do in order to sell it. When given the opportunity to vote for it, no Republican does.

If things were going well, all we'd be hearing from the fellow travelers and water carriers is about how great this Democrat health care law is doing. Because things are predictably not going well, Democrats and their allies are doing their best to pin the origin on Republicans. I guess coming up with the idea and doing nothing with it is as bad as stealing the idea and being dumb enough to vote for it? I dunno. I'm not sure what the goal here is.

Deflection and spin. Repeat the same thing often enough, it becomes the truth. Not going to work with this though.

You mean like "If you like your plan you can keep it"?

The pop-up when I enter the TalkingPointsMemo site

Tell House Republicans: We're Taking Back the House

Enough is enough. It’s time to take back the House from the extreme GOP and replace these guys with pro-choice Democratic women. Women who will step up, govern, and fight for policies that actually help women and families.

Sign up to learn how you can help us take back the House, and restore some sanity to Congress.

Talking Points Memo (or TPM) is a web-based political journalism organization created and run by Josh Marshall, a journalist, liberal blogger[2] and historian.[3] It debuted on November 12, 2000. The name is a reference to the memo (short list) with the issues (points) discussed by one's side in a debate or used to support a position taken on an issue.

When the question arose, Mr. Obama’s advisers decided that the assertion was fair, interviews with more than a dozen people involved in crafting and explaining the president’s health-care plan show. …

One former senior administration official said that as the law was being crafted by the White House and lawmakers, some White House policy advisers objected to the breadth of Mr. Obama’s “keep your plan” promise. They were overruled by political aides, the former official said. The White House said it was unaware of the objections.

The White House said it was unaware of the objections.

That seems eerily familiar........

ObamaCare - I know nothing

Benghazi - I know nothing

IRS scandal - I know nothing

NSA Spying - I know nothing

Phone tapping the media - I know nothing

Fast and Furious - I know nothing

Solyndra - I know nothing

Tapping of Merkel's phone - I know nothing

Ouze wrote: Uh, not really, no. I guess it does if you didn't read either the original article or the supporting one I linked. Are you trying to predicate that I said they probably don't pay payroll tax to pretend this indeed means all of their income is undeclared? Because... well, independant contractors aren't covered by payroll tax anyway.

If this discussion is going to devolve into single sentence Seaward-style dodges and intentionally-missing-the-points, I guess good luck with that.

So how would one go about paying payroll tax on an income derived from illegal means without further breaking the law? It seems you're the one who is trying to dodge my point about their illegal income by saying that they pay taxes elsewhere (sales tax etc.)

There is no payroll tax on independent contractors. I've said it twice now. They aren't dodging anything. I've also given you an article that clearly explains how and why sex workers can and do file federal income taxes on income from unlawful sources; mostly because the penalties for sex work are usually minor misdemeanors whereas failing to file and evading taxes are significantly more serious.

The ACORN line is a bit of a red hedding, don't you think? It's an older article that was written before it turned out that the tape was doctored. There is more to that article than a single sentence, and even if it were true, "how to file taxes" isn't really manipulating tax laws any more than, say, Google or GE or whatever company avoids paying tax on billions of dollars in income by routing it though however many countries - it's not unlawful.

This message was edited 2 times. Last update was at 2013/11/04 17:29:13

lord_blackfang wrote: Respect to the guy who subscribed just to post a massive ASCII dong in the chat and immediately get banned.

Flinty wrote: The benefit of slate is that its.actually a.rock with rock like properties. The downside is that it's a rock

The White House said it was unaware of the objections.

That seems eerily familiar........

ObamaCare - I know nothing

Benghazi - I know nothing

IRS scandal - I know nothing

NSA Spying - I know nothing

Phone tapping the media - I know nothing

Fast and Furious - I know nothing

Solyndra - I know nothing

Tapping of Merkel's phone - I know nothing

I should have went as Obama for Halloween (without the mask of course, otherwise I'm a racist) and when people asked me what my costume was I would say "I don't know"

"So, do please come along when we're promoting something new and need photos for the facebook page or to send to our regional manager, do please engage in our gaming when we're pushing something specific hard and need to get the little kiddies drifting past to want to come in an see what all the fuss is about. But otherwise, stay the feth out, you smelly, antisocial bastards, because we're scared you are going to say something that goes against our mantra of absolute devotion to the corporate motherland and we actually perceive any of you who've been gaming more than a year to be a hostile entity as you've been exposed to the internet and 'dangerous ideas'. " - MeanGreenStompa

"Then someone mentions Infinity and everyone ignores it because no one really plays it." - nkelsch

Ouze wrote: There is no payroll tax on independent contractors. I've said it twice now. They aren't dodging anything. I've also given you an article that clearly explains how and why sex workers can and do file federal income taxes on income from unlawful sources; mostly because the penalties for sex work are usually minor misdemeanors whereas failing to file and evading taxes are significantly more serious.

The ACORN line is a bit of a red hedding, don't you think? It's an older article that was written before it turned out that the tape was doctored. There is more to that article than a single sentence, and even if it were true, "how to file taxes" isn't really manipulating tax laws any more than, say, Google or GE or whatever company avoids paying tax on billions of dollars in income by routing it though however many countries - it's not unlawful.

You're assuming that I approve of others manipulating tax law too.

I like how you seem to try and say that prostitutes are simply independent contractors, or at least try and find an equivalence between them.

Are the prostitutes declaring income on their illegal activities, or related ones to skirt the law? p.s. the answer is in the article that you linked to.

Speaking of dodging Ouze;

"So pretty much the prostitutes can lie about their source of income, aren't being prosecuted by the IRS, but their tax documents can be used as evidence in a criminal trial against them. But you'd have us believe that they are somehow comparable with independent contractors. So who is dodging what again? "

I had great cancer doctors and health insurance. My plan was cancelled. Now I worry how long I'll live.

Everyone now is clamoring about Affordable Care Act winners and losers. I am one of the losers.

My grievance is not political; all my energies are directed to enjoying life and staying alive, and I have no time for politics. For almost seven years I have fought and survived stage-4 gallbladder cancer, with a five-year survival rate of less than 2% after diagnosis. I am a determined fighter and extremely lucky. But this luck may have just run out: My affordable, lifesaving medical insurance policy has been canceled effective Dec. 31.

My choice is to get coverage through the government health exchange and lose access to my cancer doctors, or pay much more for insurance outside the exchange (the quotes average 40% to 50% more) for the privilege of starting over with an unfamiliar insurance company and impaired benefits.

Countless hours searching for non-exchange plans have uncovered nothing that compares well with my existing coverage. But the greatest source of frustration is Covered California, the state's Affordable Care Act health-insurance exchange and, by some reports, one of the best such exchanges in the country. After four weeks of researching plans on the website, talking directly to government exchange counselors, insurance companies and medical providers, my insurance broker and I are as confused as ever. Time is running out and we still don't have a clue how to best proceed.

Two things have been essential in my fight to survive stage-4 cancer. The first are doctors and health teams in California and Texas: at the medical center of the University of California, San Diego, and its Moores Cancer Center; Stanford University's Cancer Institute; and the M.D. Anderson Cancer Center in Houston.

The second element essential to my fight is a United Healthcare PPO (preferred provider organization) health-insurance policy.

Since March 2007 United Healthcare has paid $1.2 million to help keep me alive, and it has never once questioned any treatment or procedure recommended by my medical team. The company pays a fair price to the doctors and hospitals, on time, and is responsive to the emergency treatment requirements of late-stage cancer. Its caring people in the claims office have been readily available to talk to me and my providers.

But in January, United Healthcare sent me a letter announcing that they were pulling out of the individual California market. The company suggested I look to Covered California starting in October.

You would think it would be simple to find a health-exchange plan that allows me, living in San Diego, to continue to see my primary oncologist at Stanford University and my primary care doctors at the University of California, San Diego. Not so. UCSD has agreed to accept only one Covered California plan—a very restrictive Anthem EPO Plan. EPO stands for exclusive provider organization, which means the plan has a small network of doctors and facilities and no out-of-network coverage (as in a preferred-provider organization plan) except for emergencies. Stanford accepts an Anthem PPO plan but it is not available for purchase in San Diego (only Anthem HMO and EPO plans are available in San Diego).

So if I go with a health-exchange plan, I must choose between Stanford and UCSD. Stanford has kept me alive—but UCSD has provided emergency and local treatment support during wretched periods of this disease, and it is where my primary-care doctors are.

Before the Affordable Care Act, health-insurance policies could not be sold across state lines; now policies sold on the Affordable Care Act exchanges may not be offered across county lines.

What happened to the president's promise, "You can keep your health plan"? Or to the promise that "You can keep your doctor"? Thanks to the law, I have been forced to give up a world-class health plan. The exchange would force me to give up a world-class physician.

For a cancer patient, medical coverage is a matter of life and death. Take away people's ability to control their medical-coverage choices and they may die. I guess that's a highly effective way to control medical costs. Perhaps that's the point.

So...lemme get this straight...

A patient whose doctors helped her to beat the odds and survive a cancer that is 98% fatal, is a patient who'd really like to keep her doctors. Right?

But she can't. As the PPACA supporters might say: "It's. The. Law."

This message was edited 1 time. Last update was at 2013/11/04 17:50:58

I had great cancer doctors and health insurance. My plan was cancelled. Now I worry how long I'll live.

Everyone now is clamoring about Affordable Care Act winners and losers. I am one of the losers.

My grievance is not political; all my energies are directed to enjoying life and staying alive, and I have no time for politics. For almost seven years I have fought and survived stage-4 gallbladder cancer, with a five-year survival rate of less than 2% after diagnosis. I am a determined fighter and extremely lucky. But this luck may have just run out: My affordable, lifesaving medical insurance policy has been canceled effective Dec. 31.

My choice is to get coverage through the government health exchange and lose access to my cancer doctors, or pay much more for insurance outside the exchange (the quotes average 40% to 50% more) for the privilege of starting over with an unfamiliar insurance company and impaired benefits.

Countless hours searching for non-exchange plans have uncovered nothing that compares well with my existing coverage. But the greatest source of frustration is Covered California, the state's Affordable Care Act health-insurance exchange and, by some reports, one of the best such exchanges in the country. After four weeks of researching plans on the website, talking directly to government exchange counselors, insurance companies and medical providers, my insurance broker and I are as confused as ever. Time is running out and we still don't have a clue how to best proceed.

Two things have been essential in my fight to survive stage-4 cancer. The first are doctors and health teams in California and Texas: at the medical center of the University of California, San Diego, and its Moores Cancer Center; Stanford University's Cancer Institute; and the M.D. Anderson Cancer Center in Houston.

The second element essential to my fight is a United Healthcare PPO (preferred provider organization) health-insurance policy.

Since March 2007 United Healthcare has paid $1.2 million to help keep me alive, and it has never once questioned any treatment or procedure recommended by my medical team. The company pays a fair price to the doctors and hospitals, on time, and is responsive to the emergency treatment requirements of late-stage cancer. Its caring people in the claims office have been readily available to talk to me and my providers.

But in January, United Healthcare sent me a letter announcing that they were pulling out of the individual California market. The company suggested I look to Covered California starting in October.

You would think it would be simple to find a health-exchange plan that allows me, living in San Diego, to continue to see my primary oncologist at Stanford University and my primary care doctors at the University of California, San Diego. Not so. UCSD has agreed to accept only one Covered California plan—a very restrictive Anthem EPO Plan. EPO stands for exclusive provider organization, which means the plan has a small network of doctors and facilities and no out-of-network coverage (as in a preferred-provider organization plan) except for emergencies. Stanford accepts an Anthem PPO plan but it is not available for purchase in San Diego (only Anthem HMO and EPO plans are available in San Diego).

So if I go with a health-exchange plan, I must choose between Stanford and UCSD. Stanford has kept me alive—but UCSD has provided emergency and local treatment support during wretched periods of this disease, and it is where my primary-care doctors are.

Before the Affordable Care Act, health-insurance policies could not be sold across state lines; now policies sold on the Affordable Care Act exchanges may not be offered across county lines.

What happened to the president's promise, "You can keep your health plan"? Or to the promise that "You can keep your doctor"? Thanks to the law, I have been forced to give up a world-class health plan. The exchange would force me to give up a world-class physician.

For a cancer patient, medical coverage is a matter of life and death. Take away people's ability to control their medical-coverage choices and they may die. I guess that's a highly effective way to control medical costs. Perhaps that's the point.

So...lemme get this straight...

A patient whose doctors helped her to beat the odds and survive a cancer that is 98% fatal, is a patient who'd really like to keep her doctors. Right?

But she can't. As the PPACA supporters might say: "It's. The. Law."

she must have been one of those people either too stupid or too lazy to understand that when the government says "you can keep your plan" what they really mean is, you can keep your plan, until we pass OB care.

Obviously it is connected to the ACA, but a comment made about the ACA regarding state action presumes that the ACA exists and therefore does not pertain to the passage of that law.

Honestly, anyone who believed, after the whole "public option" debacle, that the federal government would be able to force insurance companies to continue certain forms of coverage (a de facto public option) is either inattentive or not very bright.

.

But Sundby shouldn’t blame reform — United Healthcare dropped her coverage because they’ve struggled to compete in California’s individual health care market for years and didn’t want to pay for sicker patients like Sundby.

The company, which only had 8,000 individual policy holders in California out of the two million who participate in the market, announced (along with a second insurer, Aetna) that it would be pulling out of the individual market in May. The company could not compete with Anthem Blue Cross, Blue Shield of California and Kaiser Permanente, who control more than 80 percent of the individual market. “Over the years, it has become more difficult to administer these plans in a cost-effective way for our members,” UnitedHealth spokeswoman Cheryl Randolph explained. “We will continue to keep a major presence in California, focusing instead on large and small employers.”

The two insurers were also operating at a tax disadvantage in the state. As California Insurance Commissioner Dave Jones explained, “One of the factors I believe contributed to this decision….is the special tax break that California law gives to Anthem Blue Cross and Blue Shield, which has allowed and continues to allow those two companies to avoid paying $100 million in state taxes a year.” “Aetna and United Healthcare don’t get the special tax break provided to Anthem Blue Cross and Blue Shield, and so they faced a major competitive disadvantage in California.”

And then there is the company’s own justification for leaving. “The company’s plans reflect its concern that the first wave of newly insured customers under the law may be the costliest,” UHC Chief Executive Officer Stephen Helmsley told investors last October. “UnitedHealth will watch and see how the exchanges evolve and expects the first enrollees will have ‘a pent-up appetite’ for medical care. We are approaching them with some degree of caution because of that.”

Get that? The company packed its bags and dumped its beneficiaries because it wants its competitors to swallow the first wave of sicker enrollees only to re-enter the market later and profit from the healthy people who still haven’t signed up for coverage.

Sundby is losing her coverage and her doctors because of a business decision her insurer made within the competitive dynamics of California’s health care market. She’ll now have to enroll in a new plan that offers tighter networks of providers as a way to control health care costs and offer lower premiums. Eleven insurers are participating in Covered California and for the first time they won’t be able to deny coverage to Sundby or any other cancer patients.

The poor man really has a stake in the country. The rich man hasn't; he can go away to New Guinea in a yacht. The poor have sometimes objected to being governed badly; the rich have always objected to being governed at all

We love our superheroes because they refuse to give up on us. We can analyze them out of existence, kill them, ban them, mock them, and still they return, patiently reminding us of who we are and what we wish we could be.

"the play's the thing wherein I'll catch the conscience of the king,

"The two insurers were also operating at a tax disadvantage in the state. As California Insurance Commissioner Dave Jones explained, “One of the factors I believe contributed to this decision….is the special tax break that California law gives to Anthem Blue Cross and Blue Shield, which has allowed and continues to allow those two companies to avoid paying $100 million in state taxes a year.” “Aetna and United Healthcare don’t get the special tax break provided to Anthem Blue Cross and Blue Shield, and so they faced a major competitive disadvantage in California.”

What this means is that the Government via the PPACA chose the winners and losers for providing healthcare in California. The loser was United Healthcare and Aetna, and the winner was Anthem. They receive the subsidy, and thus end up as the only provider in the state on the exhange.

The author losing their coverage has absolutely nothing to do with the free markets or big business and everything to do with crony capitalism.

That is... if anything from ThinkProgress is accurate.

This message was edited 1 time. Last update was at 2013/11/04 19:24:52

Dreadclaw69 wrote: Speaking of dodging Ouze;

"So pretty much the prostitutes can lie about their source of income, aren't being prosecuted by the IRS, but their tax documents can be used as evidence in a criminal trial against them. But you'd have us believe that they are somehow comparable with independent contractors. So who is dodging what again? "

How are you still not getting this, if not intentionally? Sex workers do not have to lie about what they do on tax forms, and documenting "self employed" or whatever is not lying. It's not within the purview of the IRS to prosecute non-tax-related offenses.

I'm not equivocating them with independent contractors, I am telling you they fit the IRS definition.

This message was edited 1 time. Last update was at 2013/11/04 19:51:03

lord_blackfang wrote: Respect to the guy who subscribed just to post a massive ASCII dong in the chat and immediately get banned.

Flinty wrote: The benefit of slate is that its.actually a.rock with rock like properties. The downside is that it's a rock

Ouze wrote: @Dreadclaw - you're so obviously missing the point intentionally that I give up.

The point that these ladies are not correctly reporting their income because they derive it from illegal means, therefore they get subsidies to help them qualify for assistance with the ACA? No, that part I get loud and clear. That people who have an illicit source of income are better off under the ACA, even if they do pay sales tax.

You keep trying to compare illegal revenue streams with actual legal freelance work, then when that didn't work tried "well Google and GE manipulate tax law" thinking that would garner sympathy. You have obfuscated, sought false equivalence, provided evidence which undermines your own argument, dodge pertinent questions, and then attempt to say that I am missing the point intentionally?

Automatically Appended Next Post:

easysauce wrote: she must have been one of those people either too stupid or too lazy to understand that when the government says "you can keep your plan" what they really mean is, you can keep your plan, until we pass OB care.

Obviously it is connected to the ACA, but a comment made about the ACA regarding state action presumes that the ACA exists and therefore does not pertain to the passage of that law.

Honestly, anyone who believed, after the whole "public option" debacle, that the federal government would be able to force insurance companies to continue certain forms of coverage (a de facto public option) is either inattentive or not very bright..

You're also taking seriously a quote from someone who is on record saying that using government organs to specifically target your political opponents and break the law is fine so long as no one dies from it.

This message was edited 1 time. Last update was at 2013/11/04 19:51:29

You're also taking seriously a quote from someone who is on record saying that using government organs to specifically target your political opponents and break the law is fine so long as no one dies from it.

That isn't even close to the argument I was making in that thread.

This message was edited 2 times. Last update was at 2013/11/04 20:11:18

Life does not cease to be funny when people die any more than it ceases to be serious when people laugh.

You're also taking seriously a quote from someone who is on record saying that using government organs to specifically target your political opponents and break the law is fine so long as no one dies from it.

That isn't even close to the argument I was making in that thread.

dogma wrote: Also, bear in mind we're not talking about the IRS authorizing the execution of conservatives, we're talking about extra scrutiny being accorded to an application for nonprofit status. That might be annoying, but it isn't the end of the world.

So singling out groups for discriminatory treatment, breaching policy to harass them, asking them for details of social media activity and family members, passing their files onto outside parties is acceptable because no one was executed.

- accusations of targeting groups based on political opinion rather than suspicion of wrong doing. Including the breaching of IRS policy, and asking for unwarranted personal information

- a culture that enabled this across four different offices (Ohio, Cincinnati, DC and California) without there being any effective oversight that may have prevented this

- accusations that a reporter was targeted after an interview with Obama

- accusations that details of some of the groups targeted were passed to their political opponents and may have been used as ammunition during a Presidential Election

- accusations that they stole 60 million patient records that they had no legal right to view

- the possibility that those in senior positions within the IRS may have mislead Members of Congress who had previously asked about this issue

That is more than simply "annoying", no matter how much you had attempted to minimize it

The White House said it was unaware of the objections.

That seems eerily familiar........

ObamaCare - I know nothing

Benghazi - I know nothing

IRS scandal - I know nothing

NSA Spying - I know nothing

Phone tapping the media - I know nothing

Fast and Furious - I know nothing

Solyndra - I know nothing

Tapping of Merkel's phone - I know nothing

It's all that transparency, bro. Everything is so clear he can't see it. Since he got elected, his administration has been one big

You're also taking seriously a quote from someone who is on record saying that using government organs to specifically target your political opponents and break the law is fine so long as no one dies from it.

Explain to me how the above is similar to the below.

dogma wrote: Also, bear in mind we're not talking about the IRS authorizing the execution of conservatives, we're talking about extra scrutiny being accorded to an application for nonprofit status. That might be annoying, but it isn't the end of the world.

Also, bear in mind the below is not a summation of my argument in the relevant thread.

This message was edited 1 time. Last update was at 2013/11/05 01:35:02

Life does not cease to be funny when people die any more than it ceases to be serious when people laugh.

whembly wrote: Core elements? No... I disagree with that.

I think all think-tanks don't really represent their favor party at all. They're all about their agenda and using their political lobbying connections.

It depends on the think tank. Plenty of think tanks work independantly of the major parties, lobbying one or both where they can. But there are other think tanks like the Heritage Foundation, who form a very close working relationship with one party and and then work in conjunction with that party, effectively making their goals identical.

I was more alluding to the fact that the voters have real short attention spans... the failings of the PPACA is hot right now. By next November? Who knows. *shrugs* If it stays hot, then the Dems are screwed.

The Republicans will try and keep it in the news, whether or not they succeed in doing so will depend largely on ACA itself. Voter attention is only short when the issue is theoretical - something that may or may not be bad but doesn't actually impact their daily lives. If ACA really is impacting a lot of people in a negative way come November 2014 then it'll impact voting.

Holy fething hell Seb... what the feth? Did you miss all the campaign speechs.. the floor speeches... the general fething punditry throughout the crafting of this law?

Obama / Reid / Pelosi / Biden / the whole fething Demcrat caucus championed this. I know I posted plenty of youtube links supporting this.

There's such a massive difference between speaking as you must, and championing a cause. As an example, look at the invasion of Iraq. In the lead up to that war, all the major figures of the administration were getting every piece of media coverage they could, they were actively out there using any and all political goodwill they had built up to sell their argument. A year later and the admin had moved on to other priorities... you could still find plenty of media interviews as they responded to new events and new allegations, but they weren't actively campaigning on the issue.

ACA never had that first phase. Reid, Pelosi and Obama all spoke on the issue and defended the bill, but there was never any kind of active campaign to get out there and sell it.

Wait...wut? That doesn't make one iota amount of sense Seb. The Democrats needed every bit of their own party to pass it.

And you and Dogma laughed at my pass statement on how strong that Democratic party was at this time. They were all able to band together to pass this.

Yeah, eventually they were able to pass it. After an incredible amount of internal dealing and compromise in which every single one of the blue dogs had to be offered up special rules changes and brow beaten... and even then it only passed, as I already said, because the Democrats had lurched so far down the process, and the bill had been so massively politicised, that Democrats were left in a position where failing to pass a law would have been electorally disastrous.

Automatically Appended Next Post:

whembly wrote: Really... why does this matter when debating the PPACA?

Because it serves as one part of the story that establishes how ridiculous Republican opposition to this has been.

Well... sure. Newsflash... The Republican PARTY isn't "The Conservative" party. I think this is the crux of your confusion.

Dude, come on. The Republican Party is a conservative party. Note the small c, and note the same small c in my original term 'conservative policy'.

This should be basic stuff - the left wing of politics is broadly called progressive or liberal, and the right wing of politics is called conservative.

But you've been arguing that the PPACA is a Republican idea, so they must own up to it (and implying they ought to help fix it).

No, I have not argued anything like that. And now I'm left wondering if you've read anything I've posted in this thread at all.

I am saying that the ideas in ACA are from the right wing and the Republican party. This says nothing about the bill or who has to 'fix it', all it comments on is the level of honesty present in Republican opposition to the bill - it is an act of extreme political dishonesty to scaremonger about a reform that your own party was recently in favour of.

Also, the idea that someone has to 'fix' ACA is just another piece of bs in the long bs factory . In this case they're just framing the argument - assuming the contentious part to already be true - assuming that the bill needs fixing.

I can see us arguing this till we're both blue in the face.

We're not even arguing here. You're just quoting individuals bits and saying 'nuh uh' over and over again.

Nope. Still reject this premise. It's an attempt to lasso the blame game onto the GOP's lap. That's all.

In some quarters that's probably true. I don't speak for everyone. But I am telling you that there is a real meaning to the origin of the ideas in the ACA, and that meaning is to understand that GOP opposition from start to finish has been nothing but politics and nothing to do with the actual substance of the bill.

The political opportunism is there... but, that's the nature of politics. But, "intellectually bankrupt"? That's an overstatement.

Yeah, there's always opportunism. Opposition will always overstate the scale of government scandal, government will always oversell the strengths of their new legislation. That is, as you say, the nature of politics.

But it becomes disingenuous when the claims simply don't match reality any more. It is intellectually bankrupt to claim 'death panels' and 'socialisation of healthcare'.

And it becomes intellectually bankrupt when the nature of that opposition simply doesn't relate to what the party thinks of as the intellectual foundations of the party. When the party argues for free market solutions, and one is offered up, and the party freaks out and pretends it is not, that's intellectual bankruptcy.

Automatically Appended Next Post:

whembly wrote: What this means is that the Government via the PPACA chose the winners and losers for providing healthcare in California. The loser was United Healthcare and Aetna, and the winner was Anthem. They receive the subsidy, and thus end up as the only provider in the state on the exhange.

What part of "California law" confused you?

This message was edited 2 times. Last update was at 2013/11/05 02:27:41

“We may observe that the government in a civilized country is much more expensive than in a barbarous one; and when we say that one government is more expensive than another, it is the same as if we said that that one country is farther advanced in improvement than another. To say that the government is expensive and the people not oppressed is to say that the people are rich.”

Adam Smith, who must have been some kind of leftie or something.

"The two insurers were also operating at a tax disadvantage in the state. As California Insurance Commissioner Dave Jones explained, “One of the factors I believe contributed to this decision….is the special tax break that California law gives to Anthem Blue Cross and Blue Shield, which has allowed and continues to allow those two companies to avoid paying $100 million in state taxes a year.” “Aetna and United Healthcare don’t get the special tax break provided to Anthem Blue Cross and Blue Shield, and so they faced a major competitive disadvantage in California.”

What this means is that the Government via the PPACA chose the winners and losers for providing healthcare in California. The loser was United Healthcare and Aetna, and the winner was Anthem. They receive the subsidy, and thus end up as the only provider in the state on the exhange.

The author losing their coverage has absolutely nothing to do with the free markets or big business and everything to do with crony capitalism.

That is... if anything from ThinkProgress is accurate.

But it's also nothing to do with the ACA is it ?

If the act hadn't been passed -- say the Republican Operation : toys out of pram, had actually been effective due to a collapse in the fundamental workings of the material universe, this still would have/had already happened.

The poor man really has a stake in the country. The rich man hasn't; he can go away to New Guinea in a yacht. The poor have sometimes objected to being governed badly; the rich have always objected to being governed at all

We love our superheroes because they refuse to give up on us. We can analyze them out of existence, kill them, ban them, mock them, and still they return, patiently reminding us of who we are and what we wish we could be.

"the play's the thing wherein I'll catch the conscience of the king,

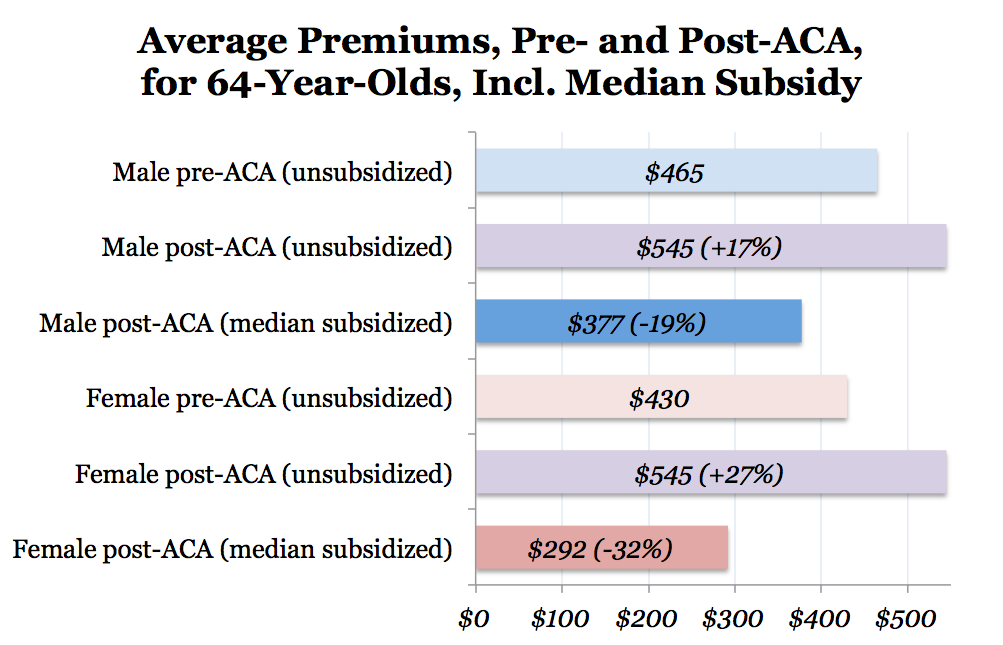

One of the fundamental flaws of the Affordable Care Act is that, despite its name, it makes health insurance more expensive. Today, the Manhattan Institute released the most comprehensive analysis yet conducted of premiums under Obamacare for people who shop for coverage on their own. Here’s what we learned. In the average state, Obamacare will increase underlying premiums by 41 percent. As we have long expected, the steepest hikes will be imposed on the healthy, the young, and the male. And Obamacare’s taxpayer-funded subsidies will primarily benefit those nearing retirement—people who, unlike the young, have had their whole lives to save for their health-care needs.

41 states, plus D.C., will experience premium hikes

If you’ve been following this space, you know that I and two of my Manhattan Institute colleagues—Yevgeniy Feyman and Paul Howard—have developed an interactive map where you can see how Obamacare affects premiums in your state. (If you ever need to find it, simply Google “Obamacare cost map.”)

In September, we released the first iteration of the map, which included data from 13 states and the District of Columbia. We only had data from a few mostly-blue states because the remainder were mostly participating in the federal exchange, and the federal exchange—for reasons we now understand more fully—hadn’t released any premium information at that time. That analysis found that underlying premiums would increase by 24 percent in those 13 states plus D.C.

Obamacare’s supporters argue that these rate increases aren’t important, because many people will be protected from them by federal subsidies. Those subsidies aren’t free—they’re paid for by taxpayers–and so it is irresponsible for people to argue that subsidies somehow make irrelevant the underlying cost of health insurance. Nonetheless, it’s important to understand the impact of subsidies on Obamacare’s exchanges; later in September, we released a second iteration of the map to do just that.

Today’s release, with the third iteration of the map, contains both premium and subsidy data for every state except Hawaii. (Believe it or not, we’ve had success mining data from every exchange website but Hawaii’s.) This nearly-complete analysis finds that the average state will face underlying premium increases of 41 percent. Men will face the steepest increases: 77, 37, and 47 percent for 27-year-olds, 40-year-olds, and 64-year-olds, respectively. Women will also face increases, but to a lesser degree: 18%, 28%, and 37% for 27-, 40-, and 64-year-olds.

Eight states will enjoy average premium reductions under Obamacare: New York (-40%), Colorado (-22%), Ohio (-21%), Massachusetts (-20%), New Jersey (-19%), New Hampshire (-18%), Rhode Island (-10%), and Indiana (-3%). Most, but not all, of these states had heavily-regulated individual insurance markets prior to Obamacare, and will therefore benefit from Obamacare’s subsidies, and especially its requirement that everyone purchase health insurance or pay a fine.

The eight states that will face the biggest increases in underlying premiums are largely southern and western states: Nevada (+179%), New Mexico (+142%), Arkansas (+138%), North Carolina (+136%), Vermont (+117%), Georgia (+92%), South Dakota (+77%), and Nebraska (+74%).

If you’re interested in more details about our methodology, you can find them here. As with our past work, we calculated an average of the five least-expensive plans in every county in a state pre-Obamacare, adjusted to take into account those with pre-existing conditions and other health problems. We then did the same calculation with the five least-expensive plans in every county in the Obamacare exchanges. We then used these county-based numbers to come up with a population-weighted state average pre- and post-Obamacare.

Exchange plans narrow your choice of doctor, despite higher costs

The key thing to understand about our before-and-after comparison is that it is an average. If you’re healthy today, you will face steeper rate increases than these figures indicate. If you have a serious medical condition, however, and haven’t been able to find affordable health coverage as a result, you will do much better under Obamacare than the average person. Men will face steeper increases than women in most states, because women consume more health care than men do, and Obamacare forbids insurers to charge different prices on the basis of gender.

In addition, our comparison ignores other differences between pre-Obamacare and post-Obamacare plans. For example, in some cases, people looking for comparably-priced coverage on the exchanges will need to accept higher deductibles and other cost-sharing arrangements.

Importantly, post-Obamacare exchange plans will typically have narrow networks of physicians and hospitals, especially excluding those tied to prestigious medical schools. In today’s Wall Street Journal, Edie Sundby, who struggles with gallbladder cancer, argues that her pre-Obamacare access to leading academic cancer centers like Stanford has “kept me alive,” and notes that the plans available to her on the exchange don’t allow her to keep her doctor.

Elderly will receive massive subsidies, thanks to younger people

Thanks to community rating, a key feature of Obamacare, insurers are only allowed to charge their oldest customers three times the amount they charge their youngest customers. Because 64-year-olds consume on average six times as much health care as 19-year-olds, this rule has the effect of driving up the cost of insurance for young people.

But there’s a double whammy. Because premiums for those nearing retirement can still be three times higher than those of younger Americans, elderly individuals will disproportionately benefit from Obamacare’s subsidies. The subsidies increase in proportion to the percentage of your income that is tied up in health insurance; for elderly people whose premiums are much higher, the subsidies are higher too.

And when I say young people, I particularly mean young men. A young woman of average income in the average state will experience little net change in premium costs, if you take subsidies into account; 40-year-old women will see an average increase of 9 percent, and 27-year-old women will see an average decrease of 5 percent. (However, as I noted above, women in good health will see meaningfully higher increases than these averages reflect.)

Let’s take the two extremes. If you’re a 27-year-old man, your average premium under our methodology, pre-Obamacare, is $133 a month. Post-Obamacare, that increases to $201. If you add in the subsidies that accrue to someone with the median income of a 27-year-old man, the net cost of Obamacare insurance goes down slightly to $188. That’s a 41 percent increase, despite the impact of subsidies.

If you’re a 64-year-old woman, on the other hand, your average pre-Obamacare premium was $430 a month. Post-Obamacare, the underlying premium increases to $545 a month. But when you factor in subsidies for the average 64-year-old woman, the net cost of Obamacare insurance drops to $292. That’s a 32 percent decrease, inclusive of subsidies, from pre-Obamacare premiums, and a 46 percent discount off of post-Obamacare prices.

The irony is that, in 2012, younger voters overwhelmingly supported President Obama, while older voters backed Mitt Romney. Obamacare, in the average state, is a massive transfer of wealth from the young to the old.

This all assumes, of course, that the exchanges eventually work

Right now, the headlines are dominated with stories about the deep and thorough dysfunction of the federally-built Obamacare insurance exchange. It’s a serious problem. If the exchanges aren’t fixed soon, the likely outcome is that older, sicker, and poorer people sign up, while everyone else goes without coverage. That, in turn, will imbalance the insurance pool in the exchanges, making its products more expensive and subsidy-dependent. Those facing cancellation of their existing coverage face the greatest risk under the worst-case scenario.

But there is a best-case scenario, especially from the standpoint of the law’s supporters. It’s that the exchanges eventually get fixed, and turn out to be popular, even among the young men—the “bros”—who bear the steepest costs under the new system. If they do, not only will Obamacare be here to stay, but the law could end up evolving into an effective replacement for our older, single-payer health-care entitlements, Medicare and Medicaid.

From where we stand today, unfortunately, there is no reason to believe that the Obama administration has a handle on the problems with the federal exchange. Young men seem no more likely to buy a costlier insurance product than they were to buy one, pre-Obamacare, that was more affordable. And so we should remain concerned about the likelihood of the law’s ultimate success.

. . .

METHODOLOGY NOTES: As noted in the text, please refer to our methodology page for a detailed description of how we arrived at these numbers. Notably, there are some quirks with the way the “Your Decision” data is displayed on the interactive map:

A few important notes are also in order. The breakeven point is only available for those states where we found rate increases for a median income household with subsidies. In states with a decrease, the inflection point is labeled with as “0…”

As of this writing, we have been unable to find data for Hawaii for datasets 1 and 2. Additionally, the average of 5 cheapest plans in Alabama ends up being more expensive than the second-cheapest silver plan (which is used to calculate subsidies). Thus, in Alabama, we assume, for the purposes of developing a net cost of insurance for the median individual, that the individual purchases the second-cheapest silver plan.

Thanks to Paul Chung, our Manhattan Institute intern, who helped us develop data-mining software that we used in this analysis. Yevgeniy Feyman led a group of PhD students who helped crunch the numbers. We collaborated with Jonathan Wu and Brian Quinn of ValuePenguin, a consumer finance website, to obtain data from certain states.

whembly wrote: Core elements? No... I disagree with that.

I think all think-tanks don't really represent their favor party at all. They're all about their agenda and using their political lobbying connections.

It depends on the think tank. Plenty of think tanks work independantly of the major parties, lobbying one or both where they can. But there are other think tanks like the Heritage Foundation, who form a very close working relationship with one party and and then work in conjunction with that party, effectively making their goals identical.

Seb... that's called lobbying.

I was more alluding to the fact that the voters have real short attention spans... the failings of the PPACA is hot right now. By next November? Who knows. *shrugs* If it stays hot, then the Dems are screwed.

The Republicans will try and keep it in the news, whether or not they succeed in doing so will depend largely on ACA itself. Voter attention is only short when the issue is theoretical - something that may or may not be bad but doesn't actually impact their daily lives. If ACA really is impacting a lot of people in a negative way come November 2014 then it'll impact voting.

meh... I'm skeptical of that. There will be a "new shiny bauble" by then.

Holy fething hell Seb... what the feth? Did you miss all the campaign speechs.. the floor speeches... the general fething punditry throughout the crafting of this law?

Obama / Reid / Pelosi / Biden / the whole fething Demcrat caucus championed this. I know I posted plenty of youtube links supporting this.

There's such a massive difference between speaking as you must, and championing a cause. As an example, look at the invasion of Iraq. In the lead up to that war, all the major figures of the administration were getting every piece of media coverage they could, they were actively out there using any and all political goodwill they had built up to sell their argument. A year later and the admin had moved on to other priorities... you could still find plenty of media interviews as they responded to new events and new allegations, but they weren't actively campaigning on the issue.

ACA never had that first phase. Reid, Pelosi and Obama all spoke on the issue and defended the bill, but there was never any kind of active campaign to get out there and sell it.

So... in other words, they weren't entirely truthful. Imagine that.

I'd posit that if they truly championed this cause, it'd never pass.

Wait...wut? That doesn't make one iota amount of sense Seb. The Democrats needed every bit of their own party to pass it.

And you and Dogma laughed at my pass statement on how strong that Democratic party was at this time. They were all able to band together to pass this.

Yeah, eventually they were able to pass it. After an incredible amount of internal dealing and compromise in which every single one of the blue dogs had to be offered up special rules changes and brow beaten... and even then it only passed, as I already said, because the Democrats had lurched so far down the process, and the bill had been so massively politicised, that Democrats were left in a position where failing to pass a law would have been electorally disastrous.

That's the byproduct of how acrimonious Congress has gotten. In that case, I'm blaming everyone for that.

Automatically Appended Next Post:

whembly wrote: Really... why does this matter when debating the PPACA?

Because it serves as one part of the story that establishes how ridiculous Republican opposition to this has been.

No, it does not. That's classic spin.

Well... sure. Newsflash... The Republican PARTY isn't "The Conservative" party. I think this is the crux of your confusion.

Dude, come on. The Republican Party is a conservative party. Note the small c, and note the same small c in my original term 'conservative policy'.

This should be basic stuff - the left wing of politics is broadly called progressive or liberal, and the right wing of politics is called conservative.

Sure... if you'd want to stereotype. But, then again, stereotyping has it's own problem.

But you've been arguing that the PPACA is a Republican idea, so they must own up to it (and implying they ought to help fix it).

No, I have not argued anything like that. And now I'm left wondering if you've read anything I've posted in this thread at all.

Sure you have... you are saying that the Republicans are being ridiculous in their oppositions since the PPACA has some concepts that were championed by an old Heritage plan. Thus, inferring that the Republicans are purely objecting for political reasons or simply that they're racist because the President is black.

I am saying that the ideas in ACA are from the right wing and the Republican party.

And I'm saying the PPACA is nothing like it... not even fething close.

This says nothing about the bill or who has to 'fix it', all it comments on is the level of honesty present in Republican opposition to the bill - it is an act of extreme political dishonesty to scaremonger about a reform that your own party was recently in favour of.

Well... I disagree.

Also, the idea that someone has to 'fix' ACA is just another piece of bs in the long bs factory . In this case they're just framing the argument - assuming the contentious part to already be true - assuming that the bill needs fixing.

So, you think everything is just peachy. Huh... Seb... you've lost it buddy.

I can see us arguing this till we're both blue in the face.

We're not even arguing here. You're just quoting individuals bits and saying 'nuh uh' over and over again.

Funny... that's how I'm seeing you.